Some not-for-profit entities will have to prepare a mandatory sustainability report

Some not-for-profit entities will have to prepare a mandatory sustainability report

With mandatory sustainability reporting now a reality for Australian entities, questions have arisen about whether and how these new rules will impact not-for-profit entities (NFPs), including clubs, community groups and industry bodies operating through companies limited by guarantee.

Who must prepare a sustainability report?

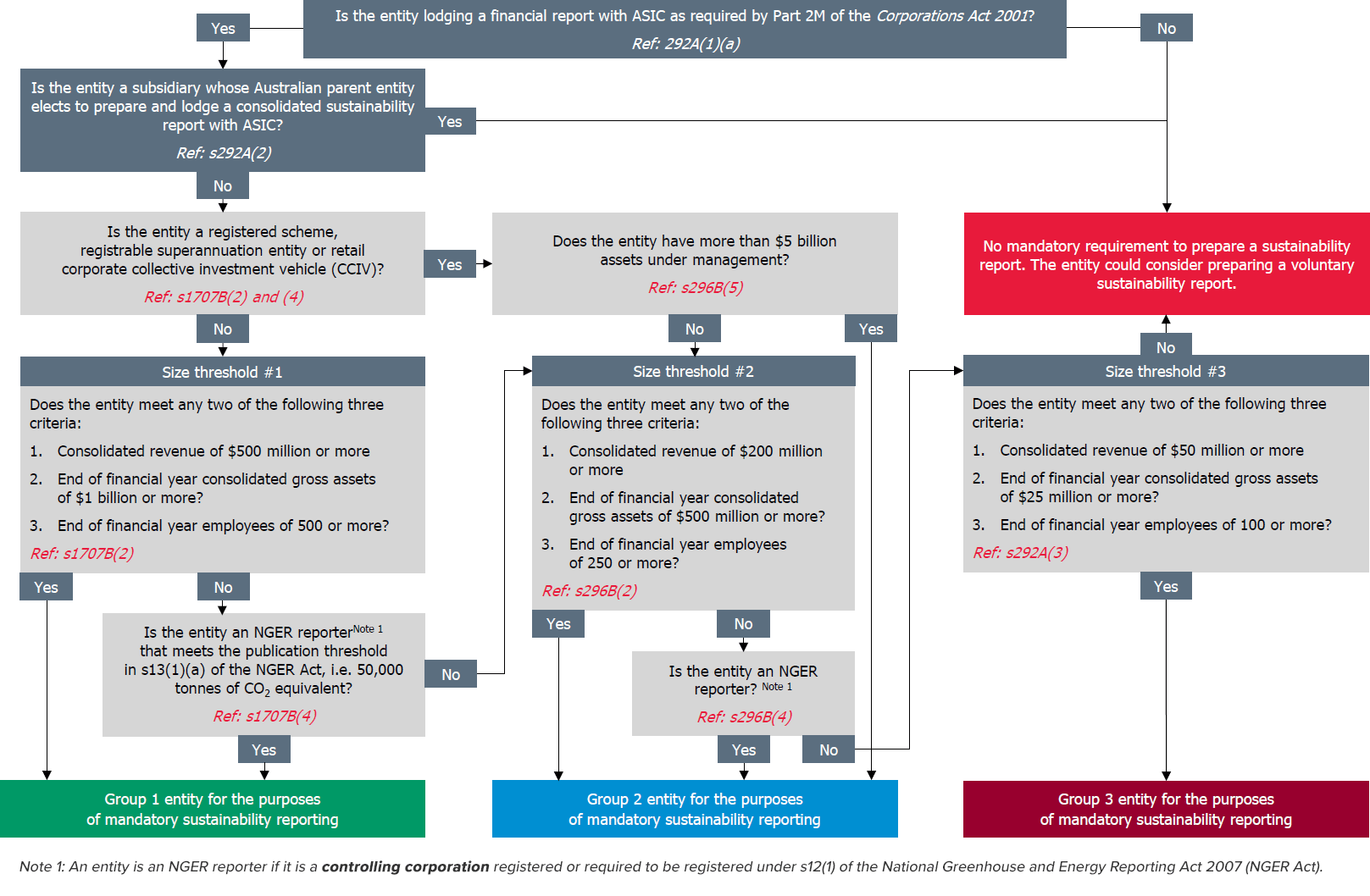

Australian entities required to prepare and lodge a financial report with the Australian Securities and Investments Commission (ASIC) under Chapter 2M of the Corporations Act 2001 must prepare a sustainability report if they meet certain criteria. The legislation requires a ‘sustainability report’, but climate-related disclosures are the first, and currently the only component of mandatory sustainability reporting.

Does this include NFPs?

NFPs structured as companies limited by guarantee may have to prepare a sustainability report if they meet certain size criteria and lodge their financial report with ASIC under Part 2M of the Corporations Act 2001. Not all companies limited by guarantee will be affected. Those registered as charities with the Australian Charities and Not-for-profits Commission (ACNC) do not lodge their financial reports with ASIC, so a sustainability report is not required.

Size criteria for mandatory sustainability reporting by certain NFPs

For NFP companies limited by guarantee that lodge their financial reports with ASIC (i.e. not registered with the ACNC), a sustainability report must be prepared if certain size thresholds are met. Our decision tree diagram below will help you determine whether your NFP is subject to mandatory sustainability reporting and, if applicable, which of the three groups it falls into.

(click to open full size)

Given that NFP companies limited by guarantee are unlikely to be ‘asset owners’ with more than $5 billion of assets under management or NGER reporters (i.e. entities required to report emissions under the National Greenhouse and Energy Reporting Act 2007), it is likely that only size thresholds #1, #2, and #3 need to be considered when determining if your NFP must prepare a sustainability report.

Types of entities most likely affected

Since sustainability reporting won’t apply to companies limited by guarantee that are charities registered with the ACNC, we expect that the types of industries most affected by the new requirements will be clubs, community groups and industry bodies operating through companies limited by guarantee.

We anticipate that many large clubs, including sporting clubs, will fall into Group 2 or Group 3 entities.

We encourage these entities to assess, sooner rather than later, whether they meet the size thresholds mentioned above, as sustainability reporting for Group 1 entities is already mandatory for 31 December 2025 year-ends.

Exceptions to mandatory sustainability reporting

NFP companies limited by guarantees controlled by for-profit entities higher up the group structure will likely opt not to prepare a separate sustainability report if an Australian parent entity prepares and lodges a consolidated sustainability report with ASIC which includes them.

When is the first sustainability report required?

The following table outlines the first mandatory reporting period end for Group 1, Group 2 and Group 3 entities with different year-ends.

|

Sustainability reports required for the first year ending on dates shown below |

|||

|

Year-end |

Group 1 entities |

Group 2 entities |

Group 3 entities |

|

31 December |

31 December 2025 |

31 December 2027 |

31 December 2028 |

|

31 March |

31 March 2026 |

31 March 2028 |

31 March 2029 |

|

30 June |

30 June 2026 |

30 June 2027 |

30 June 2028 |

|

30 September |

30 September 2026 |

30 September 2027 |

30 September 2028 |

Contents of a mandatory sustainability report

As noted above, the legislation requires a ‘sustainability report’, but climate-related disclosures are the first, and currently the only component of mandatory sustainability reporting. Climate-related disclosures are contained in AASB S2 Climate-related Disclosures (AASB S2) and include climate-related risks to which the entity is exposed (including climate-related physical risks and transition risks) and climate-related opportunities available to the entity. Disclosures are required in four sections: governance, strategy, risk management, and metrics and targets (including Scope 1, Scope 2 and Scope 3 emissions).

Measuring Scope 1, Scope 2 and Scope 3 emissions

Scopes 1, 2 and 3 emissions must be disclosed in the sustainability report, although there is an exception to defer disclosure of Scope 3 until the second year of mandatory reporting. Types of emissions by NFPs could include:

- Scope 1 emissions - for example, from natural gas usage, air conditioning, refrigeration, and fuel usage for vehicles

- Scope 2 emissions - from purchased electricity

- Scope 3 emissions - from purchased goods or services, the construction/manufacturing of capital goods (e.g. poker machines for clubs, vehicles), employees commuting to work, upstream and downstream transportation costs, waste generation, investments, etc.

Calculating emissions is a complex task, and specialist skills may be required, so we implore you to get started as soon as possible. You can reach out to our carbon accounting experts if you need help.

Get started as soon as possible

With hundreds of detailed disclosures required by AASB S2, affected NFPs will need to start preparing now for sustainability reporting. Setting a timeline or roadmap is vital to ensure your first sustainability reports are ready on time, as setting up systems and processes to measure your carbon footprint (Scope 1, Scope 2 and Scope 3 emissions) will take time.

Proactive sustainability reporting beyond climate disclosures

Embedding all aspects of Environmental, Social and Governance (ESG) principles into your entity’s strategy and operations has many benefits for NFPs.

While climate reporting is currently the only mandatory aspect of ESG reporting, the International Sustainability Standards Board is expected to publish new standards in the coming years that will encompass additional aspects of Social and Governance reporting. These are expected to be adopted in Australia. In the meantime, NFPs are encouraged to voluntarily disclose information on non-mandatory ESG topics which are material to their stakeholders and where there is a general expectation that these factors are critical to long term sustainability.

AASB S1 General Requirements for Disclosure of Sustainability-related Financial Information is a voluntary disclosure standard that can be applied to any ESG topic. Our sustainability reporting experts can help you with this process.

More information

Our previous article answers your questions about mandatory sustainability reporting, and our website contains additional resources for sustainability reporting and measuring your carbon footprint.

Need help?

Our sustainability reporting, sustainability strategy, and carbon accounting experts are on hand to assist with your sustainability reporting journey. Please contact us for help.

Subscribe to receive our insights

Subscribe