Foreign parent’s consolidated sustainability report doesn’t exempt Australian entities from sustainability reporting

Entities required to prepare a financial report under Chapter 2M of the Corporations Act 2001 must also prepare a sustainability report if they meet one of the three tests in s292A. This means, for example, that in an Australian group, the ultimate parent entity and all its subsidiaries with Chapter 2M financial reporting obligations would each have to prepare a sustainability report. This applies unless an entity is exempted by a legislative instrument from preparing financial statements, such as for wholly-owned subsidiaries, or certain small foreign-controlled proprietary companies or the exemption outlined below is applied.

Exemptions for mandatory sustainability reporting by Australian subsidiaries

S292A(2) provides an exemption to this rule. Subsidiaries will not have to prepare a separate sustainability report alongside their financial statements if the parent entity is required to prepare consolidated financial statements under Chapter 2M (i.e. they must be an Australian entity) and chooses to prepare a consolidated sustainability report for the whole group.

RG 280.45 clarifies that the exemption is only available for Australian subsidiaries where the parent entity prepares consolidated financial statements under Chapter 2M. In other words, the parent entity must be a Chapter 2M entity required to prepare consolidated financial statements for it to have the option of preparing a consolidated sustainability report.

A parent entity that is not required to prepare consolidated financial statements for the financial year under AASB 10 Consolidated Financial Statements cannot voluntarily prepare a consolidated sustainability report to avoid its subsidiaries having to prepare individual sustainability reports.

What does this mean for Australian entities with a foreign parent?

A foreign parent will not have the option to prepare a consolidated sustainability report covering all Australian subsidiaries because consolidated financial statements under Chapter 2M (for Australian financial reporting purposes) is not required.

Australian subsidiaries of foreign parent entities must, therefore, prepare an individual sustainability report under s292A unless it has an Australian parent entity that is required to prepare Chapter 2M consolidated financial statements, and the Australian parent elects to prepare a consolidated sustainability report.

Which entities will most likely be affected?

Foreign entities operating in Australia through multiple single-entry large proprietary companies are most likely to be affected because each separate entity will have to prepare its own mandatory sustainability report as illustrated in the diagram below.

.png)

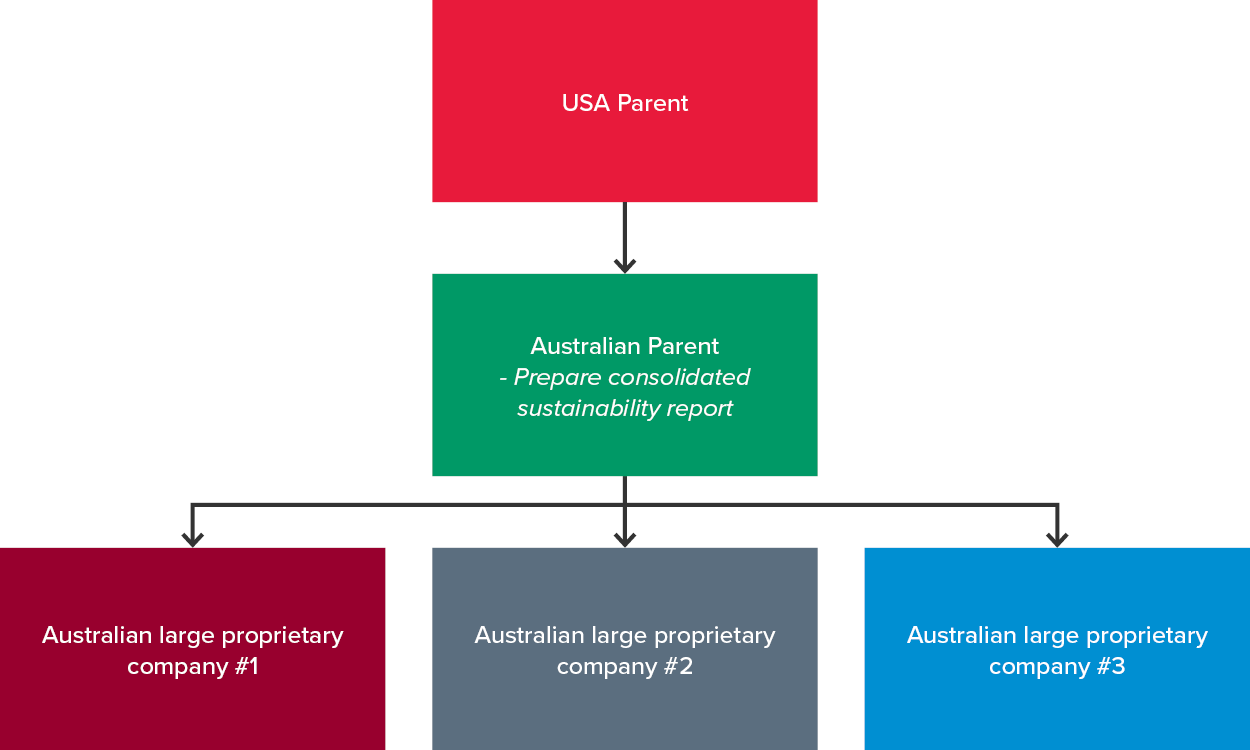

If USA Parent interposes an Australian parent, the story looks very different. As the Australian Parent is required to prepare consolidated financial statements under Chapter 2M, it can elect to prepare a consolidated sustainability report. If it chooses to do so, Australian large proprietary companies #1, #2 and #3 must each prepare and lodge financial statements (unless they are exempted by a legislative instrument from preparing financial statements), but there is no requirement for them to prepare a mandatory sustainability report if the Australian Parent chooses to prepare a consolidated sustainability report.

How can BDO help?

Operating in multiple jurisdictions? Our experts can help you track and comply with global climate reporting requirements.