What is a family office?

What is a family office?

Clients frequently ask us to define a family office and outline its services. Definitions vary, and the services can be diverse.

Broadly, a family office manages the finances, investments, governance and often the personal affairs of a wealthy individual or family. Typically, family offices are set up to oversee and preserve wealth across generations. Over the years, BDO has helped numerous family offices, each as unique as the families they serve. In our experience, a family office rarely starts from scratch; it generally evolves as various functions are established, both in-house and outsourced. While this article focuses on the financial and legal aspects of a family office, typical services that a family office could provide or be responsible for include financial services, wealth management, human resources, IT services, legal services, treasury function, governance, philanthropy, and co-ordination of family matters and events including the family council.

Key professional services of family offices

Generally, a family office will require three broad professional services: accounting, legal, and investment functions. Family offices tend to rely on a hybrid of in-house and external experts to deliver these services. In this article, we will use a worked example to explain the evolution of a family office.

A practical scenario: Navigating the evolution of a family office

Understanding the differing roles of the internal and external adviser

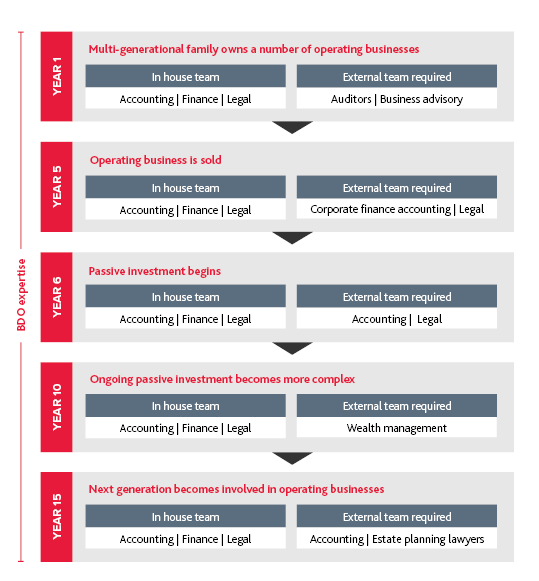

A multi-generational family owns a number of businesses through a holding company that holds shares in several operating companies. The family already has an in-house general accounting and legal team.

When one of the operating businesses is sold, the family hires external advisers—corporate finance accountants and an external corporate legal team—to assist with the sale.

After the sale, numerous fund managers approach the family to invest the surplus funds. The family invests with several different fund managers and relies on their in-house accounting team to track the investments. There is no documented policy for determining capital allocation or accessing investments at this stage.

A few years later, the investments are being tracked in a large Excel spreadsheet, which has become convoluted, difficult to digest, and no longer provides appropriate performance data. The tracking of these investments is now more prone to human error. Some investments have handed back large capital distributions, making it difficult to determine whether the portfolio performance has kept up with the broader market after fees and taxes.

Diagram: Example of a multi-generational family office over 15 years

The investment adviser

This is where our next external adviser comes in: the investment adviser. The investment adviser can use an investment platform to track and benchmark the actual performance of investments. They can also place investments through the platform, removing the legal and accounting burden from in-house professionals. This dramatically simplifies and streamlines the investment process. With technology improvements over the last few years, the price point of investment platforms has become more competitive and cheaper, while the customer experience continues to improve.

The investment adviser can also help the family draft a formal investment policy. This may be an opportunity for the next generation to become more involved in the investment process.

Later again, the next generation begins taking management positions within the remaining operating businesses. The first generation is starting to step back from operations; their mind now turns to estate planning, succession planning and family governance. The in-house legal team drafted their current planning wishes some time ago. Since then, their structure has become more complex. This may also trigger the first generation to meet with the family to discuss their legacy. Some family offices wish for an overarching entity to remain in perpetuity, while others may create multiple entities to allow for flexibility in the following generations.

Estate and succession planning

This now requires the involvement of our third set of professionals - estate planning lawyers and accountants. Of course, estate planning and succession planning should always take priority when making some of the more material decisions within the family, such as buying and selling businesses, but in our experience, it is not always front of mind.

Administrative duties

Finally, we introduce the family office’s personal affairs or administrative side. This may involve:

- Collating a monthly sweep of invoices for investment properties

- Payment of the above invoices on behalf of the client

- Payment of personal invoices

- Reporting on the performance of passive and operational assets.

Using technology and data matching, we can pay invoices to maximise interest on liquid funds and ensure payments are made in the most tax-efficient manner. Transactions can also be data-fed across investment and accounting platforms.

Expert advice to guide the development of your family office

Understanding the complexities of managing a family office can be challenging. Whether you’re just starting out or looking to optimise your existing structure, our team of family enterprise and private wealth experts are here to help. Contact us today to learn how we can support your family’s financial and personal goals, ensuring your legacy thrives for generations to come.