The first step towards a sustainability report

Stakeholders are demanding greater transparency from entities about their long-term sustainability, that is, Environmental, Social and Governance (ESG) impact. Increasingly stakeholders are questioning an organisation’s social licence to operate. This is an issue for for-profit entities because:

- Investors are directing funds preferentially (sometimes exclusively) to sustainable entities

- Financiers are facing increasing pressure to only finance sustainable entities, and

- Customers are requiring more ESG information from suppliers as whole supply chain ESG performance is having a greater impact on their purchasing decisions.

This is also an issue for not-for-profit entities, because:

- Funders and philanthropists often prioritise entities that can demonstrate a positive ESG impact, and

- Government bodies specifically fund entities that can demonstrate they achieve required outcomes and a positive impact on the community.

The future of communication to stakeholders

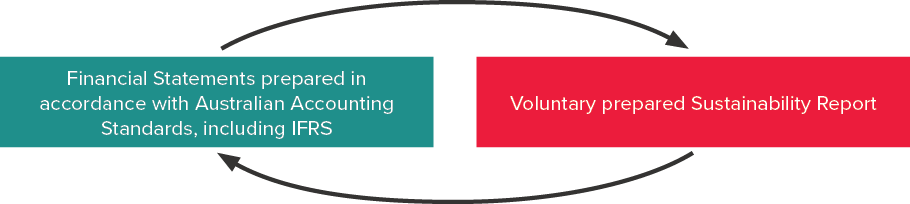

IASB and AASB’s Conceptual Framework for Financial Reporting (Conceptual Framework) issued in May 2019 states that the objective of general purpose financial reporting is to provide financial information about the reporting entity that is useful to existing and potential investors, lenders and other creditors in making informed, confident decisions when choosing to provide resources to the entity. Those decisions involve decisions about:

- buying, selling or holding equity and debt instruments;

- providing or settling loans and other forms of credit; or

- exercising rights to vote on, or otherwise influence, management’s actions that affect the use of the entity’s economic resources (Conceptual Framework paragraph 1.2).

Therefore, the primary users of general purpose financial statements are:

- Existing and potential investors

- Lenders and other creditors (Conceptual Framework paragraph 1.5).

However, the Conceptual Framework also states that general purpose financial reports do not and cannot provide all of the information that existing and potential investors, lenders and other creditors need to confidently make these critical decisions. These mission-critical enablers also need to consider pertinent information from other sources, including:

- General economic conditions and expectations

- Political events and political climate, and

- Industry and company outlooks.

The Conceptual Framework further highlights that general purpose financial statements are not designed to show the value of a reporting entity; but provide information to help existing and potential investors, lenders and other creditors estimate the value of the reporting entity. Other parties, such as regulators and members of the public (other than investors, lenders and other creditors), may also find general purpose financial reports useful even though the financial statements are not primarily directed to these parties/groups (Conceptual Framework paragraphs 1.10 and 1.11). Currently, the mandatory communication of general purpose financial statements is only directed at some of the information needs of the primary users as outlined in the Conceptual Framework.

If organisations are to prosper in this new reality where ESG matters to multiple stakeholders for multiple reasons, they must communicate their ESG impact to all stakeholders to illustrate how the organisation creates value for all stakeholders and is therefore a sustainable organisation.

The following diagram illustrates the future of integrated communication to stakeholders:

Materiality assessment

It is imperative for all organisations to identify who their stakeholders are and what information is important to them. This process is called a materiality assessment and is indeed the first step towards the preparation and publication of a sustainability report.

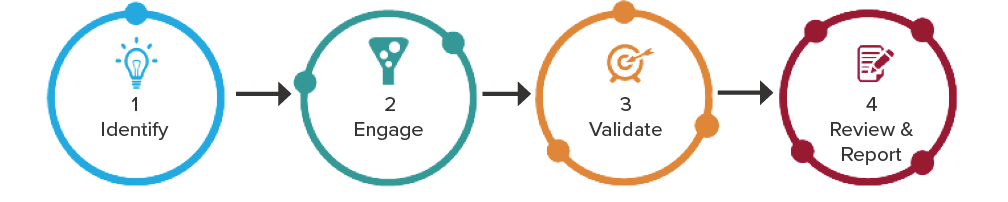

Performing a materiality assessment comprises:

- Step 1 – Identifying the stakeholders of the organisation

- Step 2 – Engaging with stakeholders to prioritise issues

- Step 3 – Validating the results with stakeholders

- Step 4 – Reviewing and finalising the materiality assessment.

Step 1 – Identify the stakeholders of the organisation

The organisation should consider all of its potential stakeholders including:

- Competitors

- Customers

- Employees

- Governments

- Investment analysts

- Investors

- Lenders

- Rating agencies

- Suppliers

- Unions.

The organisation should also identify the potentially important issues for testing with stakeholders.

Step 2 – Engage with stakeholders to prioritise issues

The organisation should engage with all the identified stakeholders in order to prioritise issues based on importance. The engagement methodology should anticipate a combination of various mediums (surveys, face-to-face interviews, workshops, etc.), depending on the nature of the relationship with the stakeholder. This includes stakeholders:

- With direct input to the organisation’s sustainability journey

- Whose opinions and guidance is highly influential to the organisation’s sustainability journey

- Whose input to the organisation’s sustainability journey would be informative and/or supplementary

- Who will be informed of the organisation’s sustainability journey, usually through formal communication/publication.

Step 3 – Validate the results with stakeholders

As part of this step, the organisation should validate the results of the prioritisation activity with identified stakeholders.

Step 4 – Review and finalise the materiality assessment

Finally, the organisations should formalise the materiality assessment into a materiality report for internal use and potentially publication.

Need assistance?

Please contact Aletta Boshoff if you want to start the journey towards the preparation of a sustainability report for your organisation.