Fair value measurement

Many entities currently preparing special purpose financial statements (SPFS) recognise assets in their statement of financial position at ‘cost’ because obtaining fair values can be a costly exercise. However, when moving to general purpose financial statements (GPFS), some balances will have to be recognised and measured at fair value.

Which Accounting Standard?

IFRS 13 Fair Value Measurement is the Accounting Standard that defines ‘fair value’. It sets out a framework for measuring ‘fair value’, and also requires disclosure about fair value measurement if full GPFS are prepared. The Simplified Disclosures GPFS contain fewer fair value disclosures than IFRS 13.

The measurement and disclosure requirements contained in IFRS 13 do not apply to share-based payments (IFRS 2 Share-based Payment) and leases (IFRS 16 Leases). They also do not apply to measurements that are similar to fair value (but which are not fair value) such as ‘net realisable value’ of inventories (IAS 2 Inventories) and ‘value in use’ (IAS 36 Impairment of Assets).

What is ‘fair value’?

Fair value is essentially an exit price, i.e. the price at which an entity expects to sell an asset or transfer a liability. It is a market-based measurement, not an entity-specific measurement. Even though observable market transactions and information may not always be available, the objective of fair value measurement is to estimate the price at which an orderly transaction would take place between market participants at measurement date under current market conditions.

Definition of ‘fair value’ in IFRS 13

If observable pricing information is not available, fair value is measured using a valuation technique that maximises the use of observable inputs and minimises the use of unobservable inputs.

Asset or liability

Fair value is measured for a particular asset or liability. Therefore, the characteristics of the asset or liability must be taken into account when determining its fair value, but only if market participants would take those characteristics into account when pricing the asset or liability at the measurement date. Characteristics could include, for example:

- The condition and location of the asset, and

- Restrictions, if any, on the sale or use of the asset.

Fair value can be determined for a:

- Stand-alone asset or liability

- Group of assets

- Group of liabilities, or

- Group of assets and liabilities (e.g. a cash-generating unit or a business).

The transaction

Fair value must be based on a price in an ‘orderly’ transaction, which assumes:

- The asset/liability has been exposed to the market for a reasonable amount of time to allow for marketing activities that are customary for such assets/liabilities, and

- The transaction is not a forced transaction, i.e. not a fire sale.

Fair value also assumes that the transaction to sell the asset or transfer the liability takes place either:

- In the principal market for the asset or liability (i.e. the market in which the entity normally transacts), or

- In the absence of a principal market, the most advantageous market.

The principal market is usually assumed to be the market in which the entity would normally enter into a transaction to sell the asset or to transfer the liability. The most advantageous market is considered where there is no principal market.

Fair value therefore represents the price in the principal market (regardless of whether that price is directly observable or estimated using another valuation technique), even if the price in a different market is potentially more advantageous at the measurement date.

Market participants

Fair value is determined using assumptions that market participants would use when pricing an asset or a liability, assuming that they act in their economic best interest. Market participants are assumed to be independent (i.e. not a related party), knowledgeable, able and willing to transact. When developing assumptions that market participants would make, specific market participants do not need to be identified. Rather, the characteristics that distinguish different types of market participants are considered for the specific asset/liability, the principal market, and the market participants with whom the entity normally transacts.

Price

As noted above, fair value is an ‘exit price’ which is not adjusted for transaction costs because transaction costs are not a characteristic of an asset or a liability. Rather, they are specific to a transaction and may differ depending on how an entity enters into a transaction for the asset or liability.

However, transaction costs do not include transport costs. Transport costs can be included in fair value if location is a characteristic of the asset (e.g. for a commodity which needs to be mined and then transported to the principal market). In such cases, the price in the principal (or most advantageous) market is adjusted for transport costs, if any, to transport the asset from its current location to that market.

Highest and best use of non-financial assets

Fair value of a non-financial asset takes into account the highest and best use by a market participant, even if the entity intends to use the asset in a different way. The entity’s current use is assumed to be highest and best use unless market or other factors suggest that a different use would maximise the fair value of the asset.

Highest and best use assumes that the use of the asset that is physically possible, legally permissible and financially feasible.

Example

Entity A operates a factory on industrial land it owns, which is adjacent to a newly proclaimed residential area. Due to the shortage of residential lots in the area, the local Council has expressed interest in rezoning and subdividing the property for residential use. The estimated selling price for individual lots are significantly higher than prices for recent sales of similar-sized industrial properties.

In this case, it is likely that the assumption regarding current use being the highest and best use is rebutted because market factors suggest that selling the property as residential property would maximise the fair value of the property. In addition, the alternate use appears to be physically possible, legally permissible, and financially feasible.

Liabilities and an entity’s own equity instruments

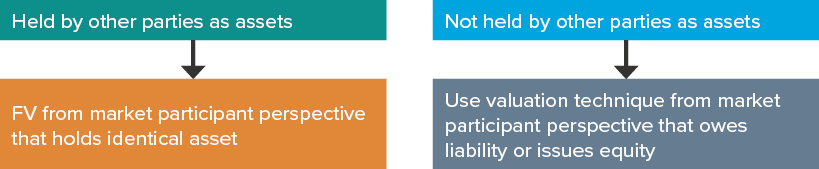

Measuring fair value for liabilities and an entity’s own equity instruments when quoted prices are not available depends on whether:

- The identical item is held by another party as an asset, or

- The identical item is not held by another party as an asset.

If the identical item is held by another party as an asset, an entity measures fair value of the liability or equity instrument from the perspective of a market participant that holds the identical item as an asset at the measurement date.

If the identical item is not held by another party as an asset, an entity measures the fair value of the liability or equity instrument using a valuation technique from the perspective of a market participant that owes the liability or has issued the claim on equity.

The following should also be noted when measuring fair value for a liability or the entity’s own equity instruments.

Non-performance risk

Firstly, the fair value of a liability must also reflect the effect of non-performance risk, including an entity’s own credit risk.

Restrictions preventing the transfer of a liability or an entity’s own equity instrument

When measuring the fair value of a liability or an entity’s own equity instrument, no separate input, or adjustment to other inputs, is made for restrictions that prevent the transfer of the item. This is because the effect of such restrictions is either implicitly or explicitly included in the other inputs to the fair value measurement.

Financial liability with a demand feature

Lastly, the fair value of a financial liability with a demand feature (e.g. a demand deposit) cannot be less than the amount payable on demand, discounted from the first date that the amount could be required to be paid.

Fair value at initial recognition

The transaction price paid to acquire the asset or received to assume the liability is an ‘entry price’ but as noted above, fair value is an ‘exit price’ and there may be a difference between the two. Entities need to determine at initial recognition whether fair value equals the transaction price, and this may not be the case if any of the following conditions exist:

- The transaction is between related parties, unless there is evidence that the transaction was entered into on market terms

- The transaction takes place under duress, or it is a ‘forced sale’ because the seller is experiencing financial difficulty

- The unit of account represented by the transaction price is different from the unit of account for the asset or liability measured at fair value, for example in a business combination

- The market in which the transaction takes place is different from the principal market (or most advantageous market). For example, a dealer enters into transactions with customers in the retail market, but the principal (or most advantageous) market for the exit transaction is with other dealers in the dealer market.

If another Accounting Standard requires or permits an entity to measure an asset or a liability initially at fair value, and the transaction price differs from fair value, the entity recognises a gain or loss in profit or loss, unless that Accounting Standard says otherwise.

Three valuation techniques

IFRS 13 does not mandate the type of valuation technique but requires that it should maximise the use of relevant observable inputs and minimise the use of unobservable inputs. The objective of a valuation technique is to estimate the price at which an orderly transaction to sell an asset or transfer a liability would take place between market participants at measurement date.

The Standard discusses three valuation techniques:

| Valuation technique | Description |

Market approach | Uses prices generated by market transactions for identical or comparable (similar) assets and liabilities |

Income approach | Converts future amounts (e.g. cash flows) into a single current discounted amount |

Cost approach | Reflects the amount that would be required to currently replace the service capacity of an asset (current replacement cost) |

Please refer to Appendix B to IFRS 13 further detail on these valuation techniques.

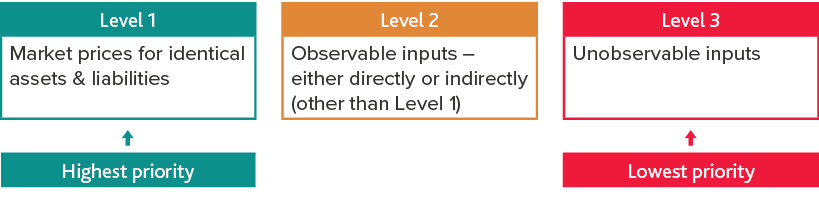

Fair value hierarchy

IFRS 13 establishes a fair value hierarchy that categorises inputs used in valuation techniques used to measure fair value as:

- Level 1 – quoted prices (unadjusted) in active markets for identical assets and liabilities (e.g. share prices on the ASX)

- Level 2 – inputs (other than quoted prices used in Level 1) that are observable for an asset or liability, either directly or indirectly

- Level 3 – unobservable inputs.

IFRS 13 does not mandate or prioritise using one valuation technique over another, however, it does prioritise which inputs to use. When determining fair value, highest priority must be given to Level 1 inputs (quoted prices) and lowest priority must be given to Level 3 (unobservable) inputs.

If there is a quoted price in an active market (Level 1 input) for an asset or a liability, that price should be used as fair value (except in very limited circumstances outlined in paragraph 79).

Disclosures

Fair value disclosures for full GPFS contained in IFRS 13 are extensive. These are not required:

- For fair value information regarding plan assets measured at fair value (IAS 19 Employee Benefits), and

- Where recoverable amount is determine using ‘fair value less costs of disposal’ (IAS 36).

Because of the uncertainty surrounding unobservable inputs (Level 3), IFRS 13 contains significantly more disclosure about Level 3 inputs than Levels 1 and 2.

Need help?

If you need help determining fair values or the appropriate fair value disclosures when preparing general purpose financial statements, please contact a member of BDO’s IFRS Advisory team. In addition, if you missed our virtual workshop on Fair value measurements - IFRS 13 and would like to purchase the recorded materials, please contact Aletta Boshoff.