Why scope and definitions matter: Enhancing financial reporting and audit quality

Why scope and definitions matter: Enhancing financial reporting and audit quality

In our previous article, we explored the benefits of accounting position papers for both management and auditors, highlighting their role in facilitating both financial reporting and audit quality. This month we explore how management and auditors’ interpretations and assessments of the scope of various IFRS® Accounting Standards and their associated definitions are critical to the preparation of accounting position papers. We will also discuss the implications for financial reporting and audit quality.

The absence of perfect accounting standards

Last month we outlined a number of reasons why accounting standards fail to provide unambiguous guidance on the appropriate accounting treatment of all feasible accounting transactions and events, including:

- The ‘Gaps in GAAP’ that typically arise from consultative standard-setting processes, and

- How changes in products and markets over time can impact the interpretation and application of principles-based accounting standards.

Consequently, preparers and auditors are often (and possibly increasingly) required to apply judgement to complex accounting transactions and events to determine and assess:

- What accounting standard, if any, applies to a particular accounting transaction or event, and

- How the particular accounting transaction or event should be accounted for under the accounting standard identified or, if no accounting standard strictly applies, the accounting policy to be developed in accordance with IAS 8/AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors.

Identifying the applicable accounting standard

Both IFRS Accounting Standards and Australian Accounting Standards (AAS) are structured as a series of ‘threshold’ questions. The first aspect to consider is the scope, which relies on definitions to distinguish between accounting transactions and events that fall under a particular standard and those that do not. This process can be thought of as ‘bucketing’ transactions and events based on their key features.

Scope

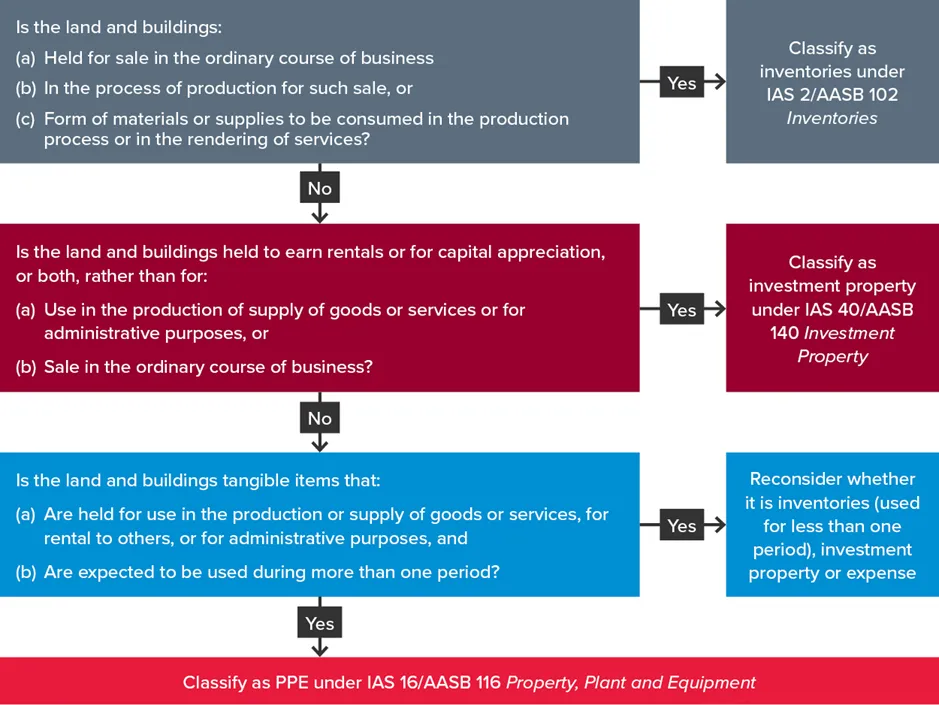

We will demonstrate this decision process using the example of land and buildings.

Every IFRS Accounting Standard and AAS has a scope paragraph. For instance, the scope paragraphs for IAS 16/AASB 116 Property, Plant and Equipment are paragraphs 2 and 3, which state:

This Standard shall be applied in accounting for property, plant and equipment except when another Standard requires or permits a different accounting treatment.

This Standard does not apply to:

(a) property, plant and equipment classified as held for sale in accordance with AASB 5 Non-current Assets Held for Sale and Discontinued Operations.

(b) biological assets related to agricultural activity other than bearer plants (see AASB 141 Agriculture). This Standard applies to bearer plants but it does not apply to the produce on bearer plants.

(c) the recognition and measurement of exploration and evaluation assets (see AASB 6 Exploration for and Evaluation of Mineral Resources).

(d) mineral rights and mineral reserves such as oil, natural gas and similar non-regenerative resources.

However, this Standard applies to property, plant and equipment used to develop or maintain the assets described in (b)–(d).

Without even knowing what ‘property, plant and equipment’ (PPE) are, it should be readily evident from the above paragraphs that:

- Only those items that are PPE are permitted to be accounted for under IAS 16/AASB 116, and

- Despite being items of PPE, some items that would otherwise fall within the scope of IAS 16/AASB 116:

- May be required to be, or the entity may have an accounting choice to, account for the item differently subject to the particular requirements of another Standard, or

- Are not permitted to be accounted for under IAS 16/AASB 116.

Unsurprisingly, this is often the first decision point where accounting errors can occur – due to insufficient attention to what is scoped in and what is scoped out of an accounting standard.

Definitions

The next decision point that can potentially result in an accounting error is an incorrect interpretation and application of the relevant definition(s). IAS 16/AASB 116 define PPE as:

...tangible items that:

(a) are held for use in the production or supply of goods or services, for rental to others, or for administrative purposes; and

(b) are expected to be used during more than one period.

Accordingly, all items that are tangible, and:

- Held for use in the production or supply of goods or services, and/or

- Held for rental to other entities, and/or

- Held for administrative purposes, and

- Were initially acquired with the expectation that they would be used over more than one reporting period,

meet the definitional criteria for classification as PPE.

While these items potentially qualify to be accounted for under IAS 16/AASB 116 because they fall within the definition of PPE, to actually fall within the scope of the PPE Standard, they must not be explicitly scoped out of IAS 16/AASB 116 (for instance, PPE classified as held for sale under IFRS 5/AASB 5). Furthermore, classification as an item of PPE doesn’t automatically result in its recognition in the entity’s statement of financial position. This only occurs after the entity has satisfied several other threshold questions around recognition and measurement.

To demonstrate some of the challenges in applying the definition of PPE, lets return to our example of land and buildings.

Land and buildings are often conceptualised as operating assets. However, land and buildings can in fact, be accounted for under IFRS Accounting Standards and AAS in at least three ways, subject to the purpose(s) for which the particular item of land and buildings are being held by the entity. The following decision tree demonstrates the notional steps through which an entity would work to establish the appropriate IFRS Accounting Standards or AAS.

While the decision tree above is based on the definitions in the applicable accounting standards, and it might seem relatively straight-forward and uncontroversial to apply, embedded within the definitions are a number of questions that are not explicitly considered in the decision tree but are, nevertheless, relevant to the correct classification of the land and buildings, including:

- What is the ‘ordinary course of business’ of the entity? For instance, if the entity has sold excess land and buildings regularly in the past, is this sufficient for all future sales of land and buildings to be considered in the ordinary course of the entity’s business (and therefore classify the land and buildings as inventories)?

- What is tangible? For instance, are leased land and buildings tangible?

- If an entity holds land and buildings to earn rentals, why would it be classified as investment property rather than as PPE? One of the key characteristics of both investment property and PPE is the asset is held to earn rentals/rental to others, and

- What if the entity has yet to determine the purpose for which the land and buildings will be held? For instance, what if the entity has not yet determined that it will use the land as owner-occupied property or for short-term sale in the ordinary course of business?

The risks of incorrectly applying an accounting standard

The purpose of the foregoing example was to demonstrate that:

- Questions of scope and definitions are a critically important first step to correctly apply accounting standards.

If an entity incorrectly concludes an accounting transaction or event should be accounted for under one standard rather than the alternative, there is a very high probability (if not, an absolute certainty) that the ultimate accounting treatment will be incorrect. For instance, it is feasible for an item of land and buildings to be incorrectly classified as investment property but accounted for consistently with PPE under IAS 40/AASB 140 using the cost model. Nevertheless, in these circumstances, the land and buildings will be incorrectly communicated to users as being held for rentals and/or capital appreciation rather than for production and/or administrative purposes. Moreover, if the entity incorrectly accounts for the land and buildings:- Under the revaluation model in IAS 40/AASB 140, it would recognise in profit or loss revaluations of the land and buildings that would not otherwise be recognised under IAS 16/AASB 116, and

- As inventories, the reported results will likely be very different to those reported under IAS 16/AASB 116

- IFRS Accounting Standards and AAS should be regarded as suites of interrelated and integrated individual standards and, therefore, should never be read and interpreted in isolation. For instance, the conclusion that an accounting transaction or event falls within the scope of one standard rather than an alternative standard requires consideration and appropriate analysis of the scope paragraphs in all of the potentially applicable accounting standards (not just the accounting standard that seemingly applies to the transaction or event), and

- The specific context of the accounting transaction or event, including the nature and objectives of the entity, and the purpose and consequences of the particular transaction or event, is critical to the correct interpretation and application of accounting standards, as demonstrated in the following table.

|

Transaction or instrument |

Context |

Applicable Accounting Standards |

|

Issued option |

To purchase issuer’s land |

AASB 138 Intangible Assets |

|

To purchase issuer’s own shares |

AASB 132 Financial Instruments: Presentation |

|

|

To employee for services |

AASB 2 Share-based Payments |

|

|

Sold a vehicle |

Part of seller’s ordinary activities |

AASB 15 Revenue from Contracts with Customers |

|

Not part of seller’s ordinary activities |

AASB 116 Property, Plant and Equipment |

|

|

Enter a supply contract for electricity that allows the buyer to fix the price of tranches |

Meets ‘own use’ criteria |

Executory contract |

|

Doesn’t meet ‘own use’ criteria |

AASB 9 Financial Instruments |

The purpose of the above table is to demonstrate how context is critical in determining the appropriate accounting standard for a particular transaction or event and, therefore, the correct classification under IFRS Accounting Standards and AAS. Accounting standards typically have different accounting requirements, including:

- Recognition requirements: Impact whether and when a transaction or event is initially recorded in the entity’s financial statements

- Measurement requirements: Affect both the initial and subsequent amounts at which the transaction or event is measured in the entity’s financial statements

- Disclosure requirements: Determine whether the transaction or event is separately presented in the entity’s financial statements and/or if further information is disclosed in the notes.

An incorrect assessment of the context of an accounting transaction or event can significantly impact financial reporting and audit quality, affecting both those charged with governance and auditors.

Next month we will take a closer look at some of the common mistakes we see regarding questions of scope and definitions in the application of IFRS Accounting Standards and AAS.

Need assistance?

BDO offers comprehensive support to entities seeking to become audit-ready or needing assistance preparing accounting position papers.

For assistance, please contact BDO’s IFRS & Corporate Reporting team.