Profit or loss statement under IFRS 18 differs for entities with specified main business activities

Profit or loss statement under IFRS 18 differs for entities with specified main business activities

IFRS 18 Presentation and Disclosure in Financial Statements is a new financial statements presentation standard that replaces IAS 1 Presentation of Financial Statements. Under IFRS 18, all entities will have to change the way they classify expenses in the statement of profit or loss, allocating them to one of five categories: investing, financing, income taxes, discontinued operations and operating. However, classification may differ, depending on whether the entity has specified main business activities. This article looks at what is meant by specified main business activities.

Why do you need to consider IFRS 18 now?

Transitioning your financial statement presentation from IAS 1 to IFRS 18 is not a simple exercise. IFRS 18 is not just about reclassifying line items. While this may be the result, how and why an entity gets to those reclassifications is challenging because IFRS 18 is a long and complex standard. Addressing the how and why involves entities making judgements regarding specified main business activities and income and expense categories. These judgements must be documented, supportable and evidenced. In addition, system changes will be required to appropriately tag expenses to the five new categories. Entities should, therefore, start their IFRS 18 implementation projects now in order to be ready to retrospectively restate comparatives from 1 January 2026. Our publication and webinar will help you on your IFRS 18 implementation journey.

Why are special rules needed for classifying income and expenses in the statement of profit or loss?

Income and expenses are generally classified into one of the five categories based on the characteristic of the expense (i.e. the type of asset or liability to which the income or expense relates). Without special rules for classifying the income and expenses of entities with specified main business activities, operating profit would not include all items of income and expenses related to the entity’s main business activities, e.g. for banks and financial institutions. IFRS 18, therefore, contains exceptions so that entities with specified main business activities will classify some income and expense items in the operating category that would otherwise have been classified in the investing and/or financing categories.

Example

Entity A sells farm equipment and provides financing to customers for the equipment sold. Both of these form part of Entity A’s main business activities. Without the exception, income and expenses from the financing side of Entity A’s business would have to be classified in the investing category, rather than the operating category.

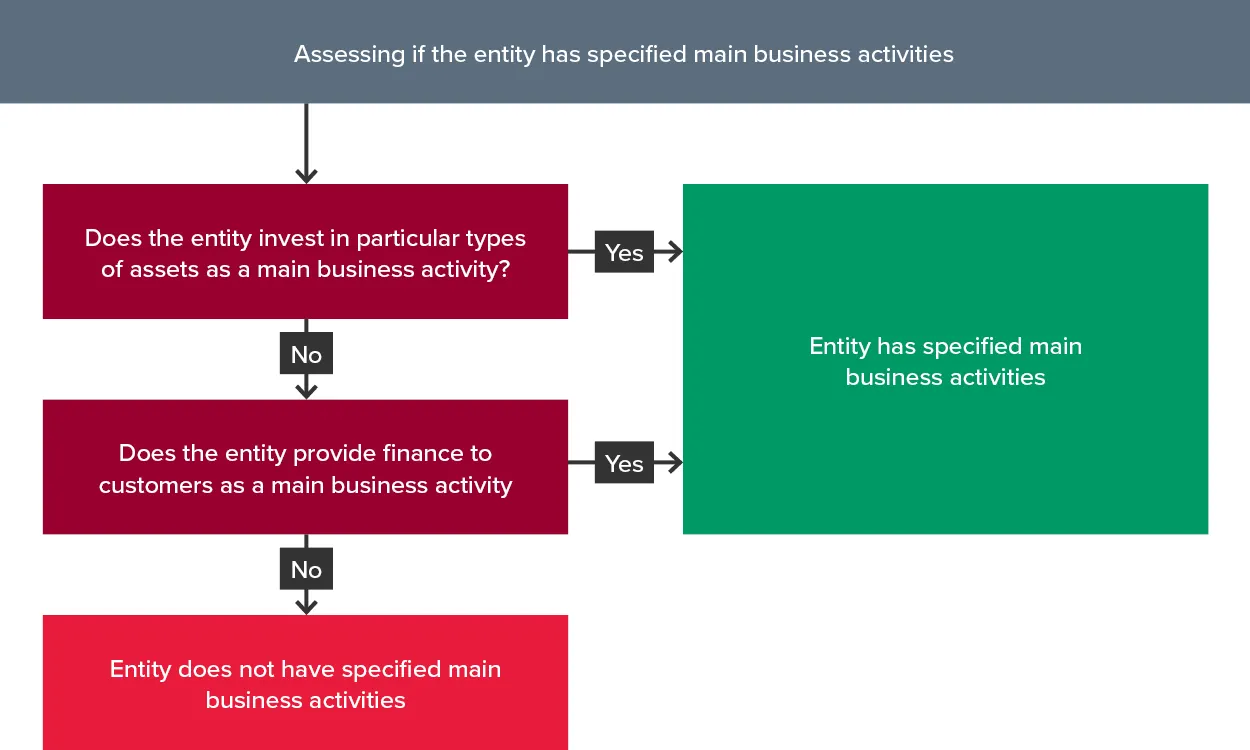

What are the specified main business activities?

IFRS 18 defines a specified main business activity as one where the main business activity of the entity is:

- Investing in particular types of assets, or

- Providing financing to customers.

In order to determine whether an entity has specified main business activities, it first needs to decide what its main business activities are. IFRS 18 does not define or explain what is meant by ‘main business activities’, so entities will need to apply judgement and should document their conclusions.

The entity must then determine whether either or both of the above (i.e. investing in assets and providing finance to customers) are its main business activities. Once one of these two criteria is met, the entity has specified main business activities. This is illustrated in the diagram below.

It is not optional for an entity to assess whether it has specified main business activities. If it has, it must apply the different classification requirements for income and expense categories.

Investing in assets

Examples of entities that might invest in assets as a main business activity include:

- Investment entities as defined by AASB 10 Consolidated Financial Statements

- Investment property companies

- Insurers.

Providing finance to customers

Examples of entities that might provide finance to customers as a main business activity include:

- Banks and other lending institutions

- Entities that provide financing to customers to enable those customers to buy the entity’s products

- Lessors that provide financing to customers in finance leases.

An example of an entity that provides financing to customers to enable those customers to buy the entity’s products is an entity that provides significant financing terms for the sale of its goods. For example, a company that sells heavy machinery may:

- Lease equipment to customers under a finance lease, or

- Legally transfer title to the equipment with a corresponding loan agreement to pay the selling entity over time through instalments of principal and interest.

The examples provided above for investing in assets and providing finance to customers are non-exhaustive - there may be many other types of entities with specified main business activities.

Judgement and evidence

Whether an entity invests in assets or provides financing to customers as a main business activity (and therefore has a specified main business activity) is a matter of fact and not merely an assertion. Entities will need to apply judgement when making this assessment, which must be based on evidence and documented. IFRS 18 notes two sources of evidence that an entity may use in assessing whether an entity has specified main business activities: the use of subtotals as an indicator of operating performance, and segment information.

The use of subtotals gives a clue to the main business activities

Certain subtotals used by an entity as important indicators of operating performance may give a clue as to what the main business activities of that entity are. An entity is likely to have a main business activity of investing in assets or providing financing to customers if:

- It uses a subtotal similar to gross profit, and

- That subtotal includes income and expenses that would otherwise be classified in the investing or financing categories if the entity did not have main business activities.

Evidence that these subtotals are important indicators of operating performance includes if the entity uses the subtotals to:

- Explain operating performance externally, or

- Assess or monitor operating performance internally.

Subtotals similar to gross profit are common in certain industries. For example, banking and lending institutions commonly use a subtotal of interest income less interest expense, which may be labelled as ‘net financial margin’ or ‘net interest income’. Use of such a subtotal in external and/or internal communications may indicate that an entity provides financing to customers as a main business activity.

Segment reporting may also give a clue to the main business activities

If an entity applies IFRS 8 Operating Segments, information reported about segments under IFRS 8 can also help to provide evidence that investing in assets or providing financing to customers is a main business activity.

- Reportable segment: If a reportable segment comprises a single business activity, this indicates that the performance of the reportable segment is an important indicator of the entity’s operating performance, and that the business activity of the reportable segment is a main business activity of the entity. This is because a reportable segment (single business activity) is an operating segment that meets the quantitative thresholds in IFRS 8 (i.e. one of the 10 per cent size tests for revenue, profit or assets is met).

It should be noted that not all reportable segments comprise a single business activity.

- Operating segment: If an operating segment comprises a single business activity, this indicates that the business activity might be a main business activity of the entity if the operating segment’s performance is an important indicator of the entity’s operating performance.

While a reportable segment comprising a single business activity is deemed by IFRS 18 to be a main business activity of the entity, the same does not apply where a non-reportable operating segment has a single business activity. This is because the operating segment is likely to be too small to be considered a main business activity. The assessment of a non-reportable operating segment’s main business activities may, therefore, be part of the evidence an entity uses to assess whether the entity has specified main business activities, but it is not definitive.

Can an entity have more than one main business activity?

Yes. An entity can have more than one main business activity. For example, an entity that manufactures a product and provides financing to customers may determine that both its manufacturing activity and customer-finance activity are main business activities, with the latter being a specified main business activity.

Level to assess specified main business activities

Once an entity has identified all its main business activities, it must then determine if it has specified main business activities. For a consolidated group, the assessment is done at the group level for the parent entity and its subsidiaries as one unit of account.

The specified main business activities for the group may not simply be the result of aggregating the specified main business activities of each entity in the group, and significant consolidation adjustments may be required. This may occur due to materiality.

Example - Consolidation adjustments required on consolidation

Fact pattern

Entity J is a holding company with no substantive operations.

Entity J has three subsidiaries:

- Entity K manufactures automotive parts

- Entity L is a private lender providing loans to customers

- Entity M is a real estate company that invests in commercial real estate for rental income and capital growth and measures the investment properties at fair value.

Entity J prepares consolidated financial statements, and Entities K, L and M prepare individual financial statements as well.

Entities K, L and M make the following assessments of whether they have specified main business activities in their individual financial statements:

|

Entity |

Does entity have specified main business activities? |

|

Entity K |

No |

|

Entity L |

Yes, providing finance to customers and investing in assets (loans receivable from customers) |

|

Entity M |

Yes, investing in assets (real estate, being investment property measured at fair value under IAS 40 Investment Property) |

At the consolidated level, Entity J assesses that it has no specified main business activities because:

- The operations of Entity K are significantly larger than Entities L and M

- Entities L and M are not reportable segments in accordance with IFRS 8 at the level of Entity J

- Subtotals similar to gross profit are not used as an important indicator of operating performance.

Assessment

The table below demonstrates that Entity L and Entity M must apply the requirements for entities with specified main business activities in their individual financial statements, but consolidation adjustments will be required because Entity J has no specified main business activities.

|

Entity |

Individual financial statements |

Consolidated financial statements |

|

Entity L |

Interest income and expenses are classified in the operating category rather than the investing and financing categories |

Reclassifies interest income and expenses from the operating category to the investing and financing categories |

|

Entity M |

Rental income and fair value gains and losses on investment property are classified in the operating category rather than the investing category |

Reclassifies rental income and fair value gains and losses on investment property from the operating category to the investing category |

This example is straightforward, however, for entities with multiple main business activities, complex structures and/or many subsidiaries, making appropriate consolidation adjustments for assessments of specified main business activities may be complex and require consolidation procedures to be adjusted (e.g. adjustments to consolidation software to allow for income and expenses to be classified into different categories at different levels of consolidation).

How to assess if investing in assets is a specified main business activity?

To determine whether an entity invests in assets as a main business activity, it must consider individual assets or a group of assets with shared characteristics.

When making this assessment for financial assets, an entity is required to use groups of financial assets that are consistent with the classes of financial assets identified by applying IFRS 7, such as investments in debt or equity instruments. When assessing whether it invests in such assets as a main business activity, an entity can reach different conclusions for these classes of assets. For example, the entity may conclude that it invests in debt instruments as a main business activity, but not equity instruments.

Investments in associates, joint ventures and unconsolidated subsidiaries

Where investments in associates, joint ventures and unconsolidated subsidiaries are accounted for using the equity method (as is the case in consolidated financial statements), no assessment has to be made regarding investing in assets as a main business activity because income and expenses for these are always classified in the investing category (refer IFRS 18, paragraph 55(a)).

However, if these investments are not accounted for using the equity method, the entity must assess whether it invests in them as a main business activity. This could occur if:

- An investment entity invests in associates and joint ventures together with subsidiaries as a main business activity

- A venture capital organisation invests in associates and joint ventures as a main business activity and elects not to apply the equity method.

This assessment is performed by using individual assets or groups of assets with shared characteristics. Therefore, it is possible for an entity to conclude that it invests in certain associates, joint ventures and unconsolidated subsidiaries as a main business activity, but not others.

If an entity prepares separate financial statements under AASB 127 Separate Financial Statements and performs the assessment for groups of assets, it must use groups of assets consistent with the measurement categories in paragraph 10 of AASB 127, i.e., cost, or in accordance with IFRS 9 Financial Instruments (which would usually be fair value).

More information

Stay tuned for future Corporate Reporting Insights during 2025 as we continue our deep dive into IFRS 18 to demystify some of its complexities.

Need help

Determining whether your entity has specified main business activities is just one very small aspect of implementing IFRS 18. Implementing new accounting standards can be challenging. Reach out to our team for help with understanding the latest requirements in IFRS 18.