AASB adds sustainability reporting to its work plan

AASB adds sustainability reporting to its work plan

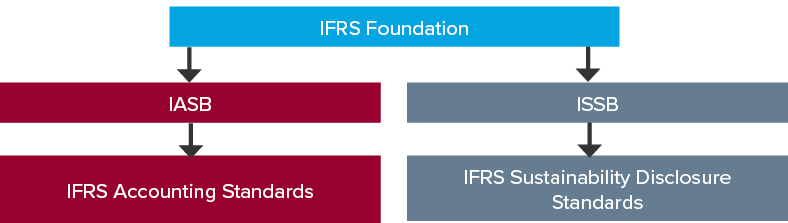

The demand for a globally consistent set of sustainability reporting standards has become a top priority for investors and various levels of government around the world. This resulted in the formation of the International Sustainability Standards Board (ISSB) in November 2021, a sibling Board to the International Accounting Standards Board (IASB), both under the governance structure of the IFRS Foundation.

The ISSB will build on the work done by previous organisations and begin issuing a single set of globally consistent sustainability standards as a ‘global baseline’.

What does this mean for Australian entities?

Jurisdictions will likely use this consistent baseline and build additional local sustainability reporting requirements where necessary. The Australian Accounting Standards Board (AASB) would therefore be required to add/amend these ‘global baseline’ standards to cater for Australian-specific requirements (in a similar way to how the AASB adds not-for-profit-specific accounting requirements to accounting standards).

The project plan

To facilitate this process, and following feedback received from its 2022-2026 agenda consultation, at its February 2022 Board meeting the AASB decided to add a sustainability project to its work program. It noted that the following should be a priority when developing the draft project plan:

- The positioning of the sustainability reporting requirements in the Australian reporting environment (i.e. where do they fit in?)

- Clearly defining the scope of work on sustainability reporting.

The following preliminary decisions were made to help AASB staff develop a draft project plan:

- The ISSB work should be used as a foundation, with modifications made only for Australian matters and requirements to meet the needs of Australian stakeholders

- It is important to leverage the work of existing sustainability reporting standard-setters and framework providers when developing modifications for Australia-specific circumstances

- The initial scope of the project is for for-profit entities of all sizes, not just larger listed entities. The not-for-profit sector will be considered at a later stage.

More information

For a ‘snapshot’ of sustainability reporting developments as at 31 December 2021, please refer to our 31 December 2021 year-end sustainability reporting update.

Need assistance with your sustainability report?

While we are waiting for the ISSB to issue globally consistent sustainability reporting standards, there are several sustainability reporting frameworks businesses can use in the meantime to draft their sustainability reports. Please contact Aletta Boshoff (Partner, National Leader, IFRS & Corporate Reporting and National Leader, ESG & Sustainability) if you require assistance with your sustainability reporting journey.