International Sustainability Standards Board launched at COP 26

On 3 November 2021, the IFRS Foundation Trustees announced three significant developments at the COP26 UN global summit in Glasgow, Scotland:

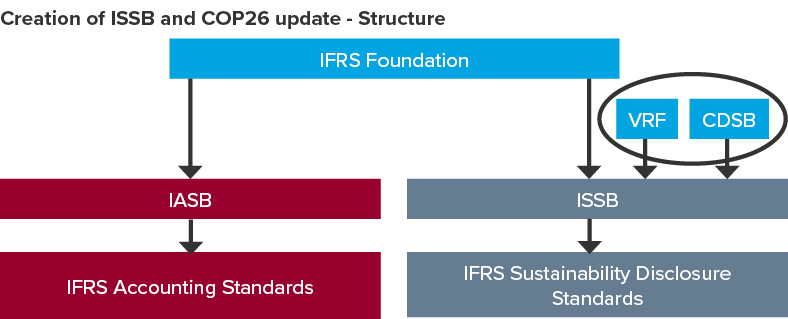

- The formation of a new International Sustainability Standards Board (ISSB), which will develop a comprehensive global baseline of high-quality sustainability disclosure standards with an aim to meet investors’ information needs

- A consolidation of the Climate Disclosure Standards Board (CDSB) and the Value Reporting Foundation (VRF – which houses the current Integrated Reporting Framework and SASB standards) into the ISSB by June 2022, and

- The publication of two prototype standards: one on climate and the other on general disclosure requirements. These prototype standards were developed by the Technical Readiness Working Group (TRWG) prior to the formation of the ISSB.

How will the ISSB interact with the International Accounting Standards Board (IASB)?

The ISSB will sit alongside the IASB under the oversight of the Trustees of the IFRS Foundation and the Monitoring Board. The IFRS Foundation Constitution has been amended to reflect this. The boards will seek to ensure connectivity and compatibility between IFRS Accounting Standards issued by the IASB and IFRS Sustainability Disclosure Standards issued by the ISSB.

Why was the ISSB formed?

There is a proven demand for information relating to environmental, social and governance (ESG) issues as these factors affect enterprise value. However, despite this demand, no consistent, globally accepted framework for disclosing this information has emerged. Many of these frameworks are voluntary, which has increased fragmentation in reporting. This has led to calls for the IFRS Foundation to form a global standard setter to increase the consistency in the reporting of this type of information, as has been accomplished by the IASB in terms of financial reporting. The creation of the ISSB follows extensive public consultation and is with the support of various regulatory bodies, including the International Organisation of Securities Commissions (IOSCO).

What are the objectives of the ISSB?

The ISSB will issue IFRS Sustainability Disclosure Standards, which will set out disclosure requirements that address entities’ impacts on sustainability matters that affect enterprise value and how investors make decisions. While the IASB issues standards that assist investors in making decisions related to financial information (e.g. profit, liquidity, etc.), IFRS Sustainability Disclosure Standards will provide investors with information on a broader set of metrics, such as the effect an entity has on climate, fresh water supplies, soil erosion, equitable treatment of employees, gender pay disparity, etc.

How will the ISSB take account of what has been issued already by other standard setters?

While the ISSB seeks to issue a set of globally accepted standards for sustainability disclosures, the board is also seeking to build upon what has already been done. In order to accomplish this, the ISSB will consolidate and merge with two existing organisations:

- The Climate Disclosure Standards Board (CDSB), and

- The Value Reporting Foundation (VRF – which houses the Integrated Reporting Framework and SASB standards).

The technical standards and frameworks established by these organisations, along with the recommendations of the Task Force on Climate-Related Financial Disclosures (TCFD) and the World Economic Forum Stakeholder Capitalism Metrics form the basis for the work to be carried out by the new Board.

What are the prototype standards and what is the ISSB expected to do with them?

The prototype standards released by the ISSB were prepared by the Technical Readiness Working Group (TRWG) to enable the ISSB to have a ‘running start’ in drafting the most pressing disclosure requirements, which are:

- General requirements for disclosure of sustainability-related financial information, and

- Climate-related disclosure.

The prototype standards provide recommendations to the ISSB for consideration in issuing eventual final standards. The prototype standards can be accessed here. While the recommendations build on the established work of the organisations represented on the TRWG, the prototype standards have not been subject to the due process of those organisations or of the IFRS Foundation. After starting its work, the ISSB is expected to consult publicly on proposals that are informed by the TRWG’s recommendations. The ISSB’s work will be subject to the IFRS Foundation’s due process.

You can read more about the above in our INTERNATIONAL SUSTAINABILITY REPORTING BULLETIN.

If you need assistance, please contact Aletta Boshoff.