SAAS implementation costs – Do you need to write these off at 30 June 2021?

Entities using cloud-based software in a Software as a Service (SaaS) arrangement may incur significant costs in relation to configuration and customisation of the supplier’s application software to which they receives access.

SaaS arrangements are usually accounted for as service contracts and not intangible assets (refer IFRIC agenda decision – March 2019). Despite no intangible asset being recognised on the balance sheet for the SaaS arrangement, some companies have nevertheless capitalised configuration and customisation costs relating to these arrangements as ‘intangible assets’. This is all about to change! For 30 June 2021, many companies may need to remove these capitalised costs from their balance sheets, and retrospective adjustments will be required to prior year comparative information.

Fact pattern

In April 2021, the IFRS Interpretations Committee (IFRIC) published its final agenda decision on accounting for configuration and customisation costs in a SaaS arrangement. The agenda decision relates to a fact pattern where:

- The SaaS arrangement gives the customer the right to receive access to the supplier’s application software over the contract term (i.e. it is a service contract and not an intangible asset)

- Configuration costs and customisation costs are incurred as described below, and

- The customer receives no other goods and services.

Configuration

Configuration involves the setting of various ‘flags’ or ‘switches’ within the application software, or defining values or parameters, to set up the software’s existing code to function in a specified way.

Customisation

Customisation involves modifying the software code in the application or writing additional code. Customisation generally changes, or creates additional, functionalities within the software.

Extracted from IFRIC final agenda decision April 2021

IFRIC considered two questions in relation to this fact pattern:

- Does the customer recognise an intangible asset in relation to these configuration and customisation costs?

- If an intangible asset is not recognised, how does the customer account for these costs?

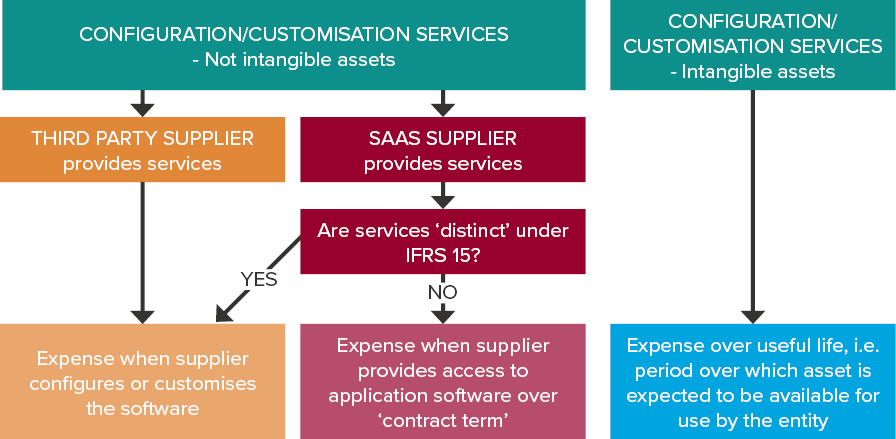

The diagram below summarises the accounting outcomes for configuration and customisation costs noted in the final agenda decision. Please read the remainder of the article for a summary of the IFRIC’s observations.

Question 1: Does the customer recognise an intangible asset in relation to these configuration and customisation costs?

It depends. In order to recognise an intangible asset for the configuration and customisation costs, the customer would need to demonstrate that each type of cost:

- Meets the definition of an ‘intangible asset’, and

- Meets the recognition criteria for an intangible asset in paragraphs 21–23 of IAS 38 Intangible Assets.

Definition of ‘intangible asset’

IAS 38 defines an intangible asset as ‘an identifiable non-monetary asset without physical substance’ and notes than an asset is a resource controlled by an entity. An entity controls an asset if it has ‘the power to obtain the future economic benefits flowing from the underlying resource and to restrict the access of others to those benefits’ (IAS 38, paragraph 13).

When determining whether configuration or customisation costs meet the definition of an ‘intangible asset’, this may depend on the nature and output of the configuration or customisation performed. The IFRIC noted in this regard:

- If the customer does not recognise an intangible asset because it does not control the application software being configured or customised - those configuration or customisation activities do not create a resource controlled by the customer that is separate from the software, and

- Some arrangements may result in additional code that the customer may control (i.e. it has the power to obtain the future economic benefits and to restrict others from having access to those benefits). In such cases, the customer considers whether other aspects of the definition of an intangible asset are met, i.e. whether the additional code is identifiable and meets the recognition criteria in IAS 38.

Question 2: If an intangible asset is not recognised, how does the customer account for these costs?

Expense when services are received as per the contract

The IFRIC observed that if an intangible asset is not recognised for the configuration or customisation costs, the customer recognises those costs in the financial statements as an expense when it receives the configuration or customisation services (IAS 38, paragraph 69). IAS 38, paragraph 69A further notes that services are received when they are performed by a supplier in accordance with a contract to deliver them to the entity, and not when the entity uses them to deliver another service.

Look to IFRS 15 for guidance on identifying the services received, and when the services are delivered to the customer

IAS 38 does not provide guidance on how to identify the services received by the customer, nor when those services have been performed by the supplier in accordance with the contract. IFRIC therefore noted that applying the hierarchy in IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors (paragraphs 10-11), we should refer to IFRS 15 Revenue from Contracts with Customers as an IFRS standard dealing with similar and related issues. IFRS 15 includes requirements for suppliers to identify:

- The promised configuration or customisation services in a contract with a customer, and

- When the supplier performs those services in accordance with the contract.

SOFTWARE SUPPLIER performs configuration and customisation services

If the customer enters into a contract with the supplier of the application software to deliver the configuration or customisation services (including where the supplier subcontracts services to a third party), the customer applies paragraphs 69–69A of IAS 38 and determines when the supplier performs those services in accordance with the contract. In this regard:

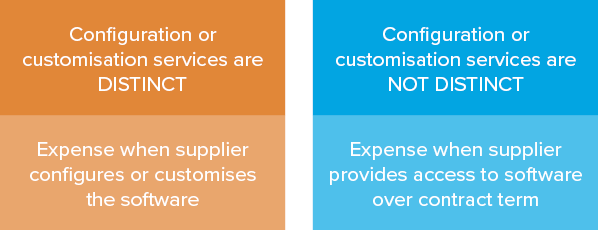

- If the services the customer receives are distinct - customer recognises the costs as an expense when the supplier configures or customises the application software.

- If the services the customer receives are not distinct (i.e. they are not separately identifiable from the customer’s right to receive access to the supplier’s application software) - customer recognises the costs as an expense when the supplier provides access to the application software over the contract term.

THIRD PARTY SUPPLIER performs configuration and customisation services

If the contract to deliver the configuration or customisation services is with a party other than the software supplier (third party supplier), the customer applies paragraphs 69–69A of IAS 38 and determines when the third party supplier performs those services in accordance with the contract.

The customer then expenses the configuration or customisation costs when the third party supplier configures or customises the application software.

Prepayments

If the customer pays for configuration or customisation service in advance of receiving those services, it recognises the prepayment as an asset.

Disclosure

The final agenda decision also reminds preparers that customers should disclose the accounting policy for accounting for configuration and customisation costs when relevant to an understanding of the financial statements (IAS 1 Presentation of Financial Statements, paragraphs 117-124).

IFRIC conclusion

IFRIC decided that neither an Interpretation nor amendments to standards is required because the principles and requirements in IFRS Standards provide an adequate basis for a customer to determine its accounting for configuration or customisation costs incurred in relation to the SaaS arrangement described in the request.

Implications for 30 June 2021 financial statements

Customers with similar SaaS arrangements will need to consider Questions 1 and 2 above in relation to material configuration and customisation costs incurred. This includes revisiting the accounting treatment of all configuration and customisation costs incurred in prior years.

Voluntary change in accounting policy

Where the customer needs to change its accounting policy for configuration or customisation costs as a result of this agenda decision, this can usually be treated as a voluntary change in an accounting policy under IAS 8, and comparatives will need to be restated accordingly.

Don’t forget the third balance sheet

Where adjustments are required to derecognise intangible assets (or in rare cases to capitalise intangible assets that were previously written off), entities should remember that a ‘third balance sheet’ as at the beginning of the comparative period is required where there are material retrospective adjustments that affect periods before the start of the comparative period.

What is the ‘contract term’ for expensing when SaaS supplier provides configuration/customisation services that are NOT DISTINCT?

When configuration or customisation services are delivered by the SaaS supplier and are not distinct, they must be expensed when the supplier provides access to the software over the ‘contract term’. It is not clear whether the ‘contract term’ is determined:

- Based on the period in which parties to the contract have enforceable rights and obligations (refer IFRS 15, paragraphs 10-12), or

- By considering the substance of the arrangement and the period over which the customer is likely to access the software (refer IFRS 15, paragraphs 95(a) and 99).

Note:

IFRS Interpretations Committee (the Committee) agenda decisions are those issues that the Committee decided not to take onto its agenda. Although not authoritative guidance, in practice they are regarded as being highly persuasive, and all entities reporting under IFRS should be aware of these decisions because they could impact the way particular transactions and balances are accounted for.

eLearning

Please click here for access to more eLearning resources.